The maximum amount you may borrow when you obtain a mortgage is 2024. Your creditworthiness and monthly disposable income are two particular criteria that will affect this. The maximum amount of money lenders in the sector can lend to borrowers for their loans to satisfy Federal Housing Finance Agency requirements is limited. The government is preparing to raise the mortgage loan limits in 2024, which will happen shortly. This blog makes knowing about this software easier.

Mortgage Loan Limit 2024:

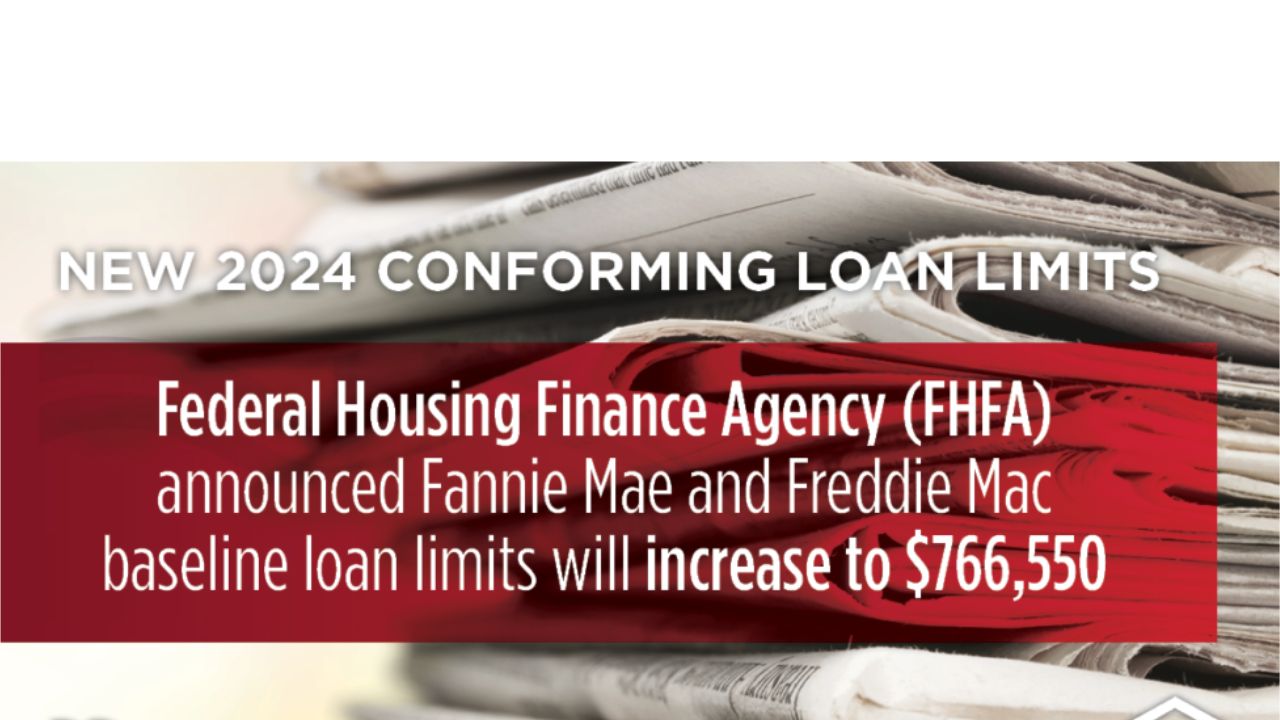

The FHFA sets conforming lending restrictions for Freddie Mac and Fannie Mae, the two government-sponsored enterprises under its supervision. Fannie Mae and Freddie purchase mortgages from lenders that meet their criteria, repackaging them into securities backed by mortgages for investors.

Thanks to this procedure, lenders now have the cash to continue providing mortgage loans to house purchasers at competitive rates. Additional requirements for loans that Fannie Mae and Freddie Mac buy include minimum down payments, minimum credit scores, and maximum debt-to-income ratios (DTI).

However, when discussing conforming loan criteria, Mortgage Loan Limit 2024 is generally expected to be comprehended. These include the borrower’s credit score as low as 620, the maximum debt-to-income ratio (DTI) of 50%, and the minimum down payment of three percent or more for the original amount. However, when most young people discuss traditional loans, they bring up these lending restrictions.

Increase in Mortgage Loan Limits Anticipated:

The restrictions for conforming loans are affected by changes in property values. Every year, the FHFA uses information from its House Price Index (HPI) report to increase its base loan limit. The HPI study calculates the Expected Raise in Mortgage Loan Limits in 2024.

New loan ceilings are set annually using third-quarter information from the FHFA House Price Index (HPI). According to Rocket Mortgage, growth will be at 5.56% in 2024.

Establishing a single conforming loan ceiling for the whole nation presents a hurdle, as it is impossible to compare property values across rural Ohio communities and Manhattan, one of the country’s most expensive real estate markets. This leads to a higher ceiling on loans set by the FHFA in regions it deems “high cost,” a categorization based on the area’s median house value about the base conforming loan limit.

Assume you are considering buying a $800,000 house in sunny California. You would need a jumbo loan if you purchase a home in San Bernardino County, which isn’t on the FHFA’s list of high-cost places. Why? When the expense exceeds the $726,200 conforming loan cap.

But what would happen if you looked in the wealthy Los Angeles County? The FHFA often sets higher loan restrictions due to the high median property value. A single-unit home’s top bound may be close to $1,089,300. A suggests you buy a $800,000 house without needing a jumbo loan.

One interesting thing to note is that not all high-cost localities have maximum loan limitations. Regardless of the number of units in the house, Alaska and Hawaii are included in the High-Cost Area Limits 2024.

What does “jumbo loan” imply in your money, then? To begin with, the upfront expenses are steep. While traditional mortgage loans may enable you to pay as little as 3% upfront, most jumbo loan applicants must pay at least 20%. Furthermore, they usually demand a minimum credit score in the 700s and a debt-to-income ratio (DTI) of less than 45%.

If this is agreeable, taking out a jumbo loan can be brilliant. Before you begin looking for a house, understand the differences between a standard and non-standard loan for your budget and know the lending constraints in your region.

To Know More Latest Finance News then Visit – stevedigioia.com